Welcome to our video outlining some of the key risks associated with virtual power purchase agreements.

Market Price Risk

The first and most significant risk is market price risk, which occurs when a company’s contracted annual renewable generation volume doesn’t align with its annual energy consumption. The greater the mismatch, the greater the company’s exposure.

If market prices are higher than expected and a company’s load over the year exceeds the generation it has purchased, the company may need to buy additional energy at high prices to meet its needs. Conversely, if market prices are lower than anticipated and the company’s load is less than the generation it has purchased, the company may find itself selling excess energy at market rates below the contracted energy price.

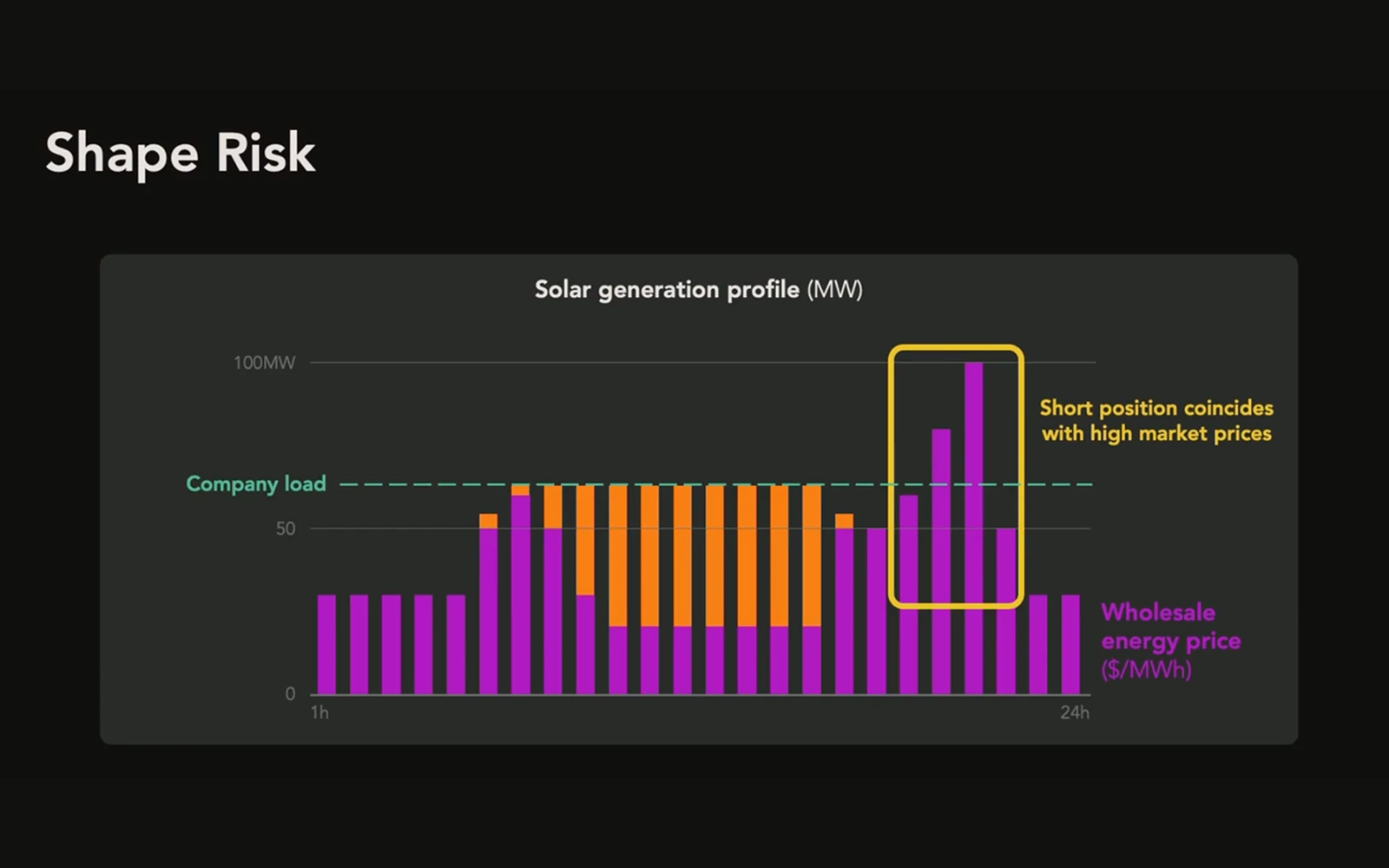

Shape Risk

Shape risk occurs when a company’s contracted hourly renewable generation volume doesn’t match its hourly energy consumption. The power output from wind and solar resources often doesn’t align with the demand profile of the energy consumer.

For example, solar power production peaks during midday, but a company may need electricity in the evening when solar generation is low or non-existent and market prices are often high. If the energy consumer’s short position coincides with high market prices, that can create significant financial risk for its clean energy portfolio.

Basis Risk

Basis risk arises when the price used to settle the vPPA differs from the price used to settle the load. For instance, if a company based in Houston enters a vPPA for a wind farm in West Texas, the settlement price for the generation at the ERCOT West trading hub can vary significantly from the settlement price for the company’s consumption at the ERCOT Houston load zone. This discrepancy can create greater financial uncertainty than if the vPPA were signed in the same region as the load.

Basis Timing Risk

Basis timing risk occurs when the market used to settle a vPPA — for instance, the real-time market — differs from the market used to settle a company’s load — for instance, the day-ahead market. This timing difference can erode the hedging effectiveness of the vPPA and create financial volatility for the energy portfolio.

For example, consider a company with a retail agreement that settles in the day-ahead market while simultaneously holding a vPPA with a solar project that settles in the real-time market. A forecasted heat wave results in high day-ahead prices — say $200 per megawatt-hour — applied to the load. But if the heat wave doesn’t materialize and real-time prices settle much lower — say $50 per megawatt-hour — even a perfectly matched vPPA volume would result in $150 per megawatt-hour in extra costs due to the timing mismatch alone.

Summary

While vPPAs offer a compelling way to invest in clean energy, it’s crucial to understand these key risks before entering a contract — so you can make data-driven decisions about pricing and risk allocation. At Verse, we help you navigate these complexities with confidence and make the most informed decisions to optimize your clean energy investments.

For more information, visit our website or contact us directly.