Here’s the cleaned-up transcript:

Welcome to our video on short-term risk management for clean energy portfolios.

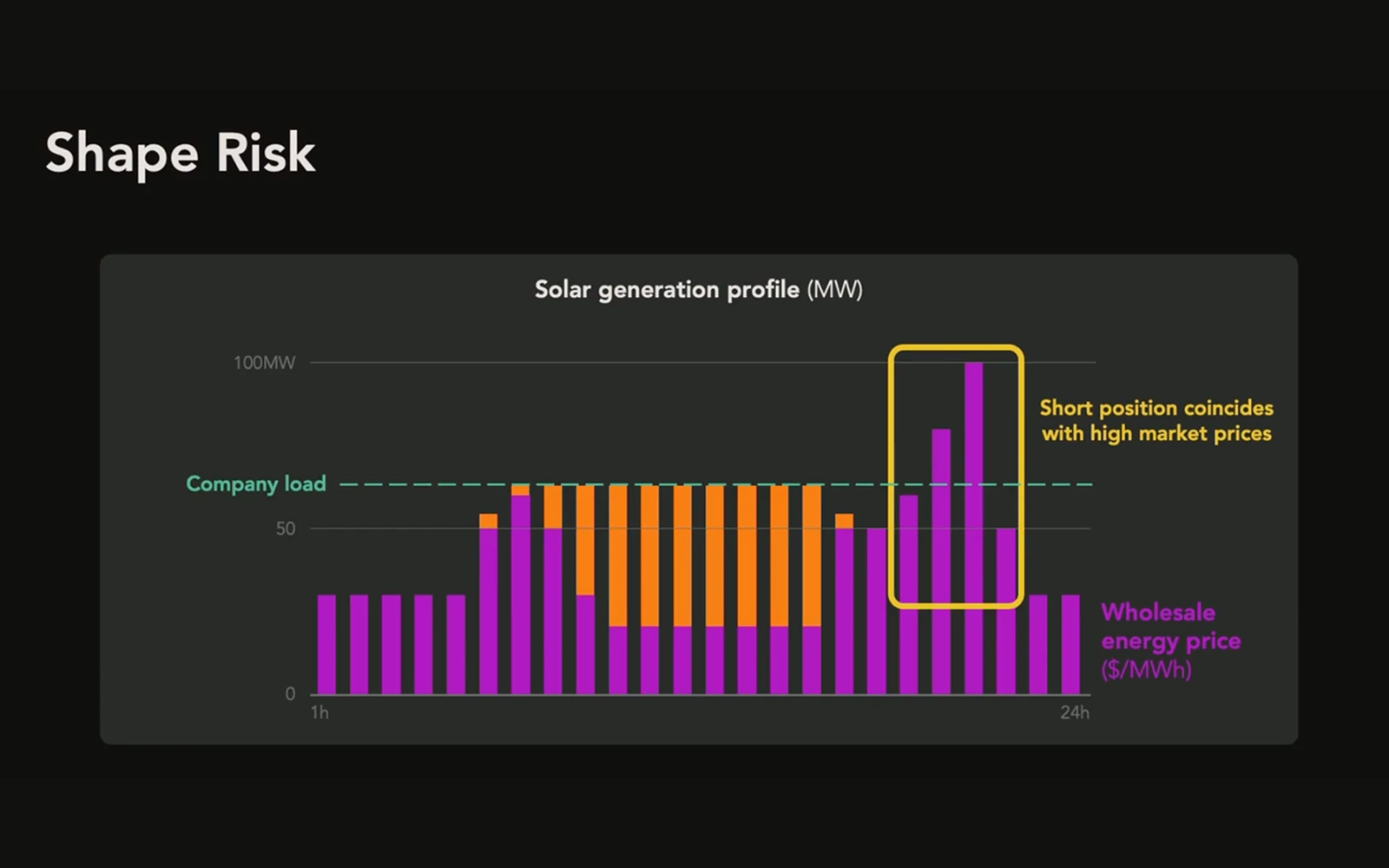

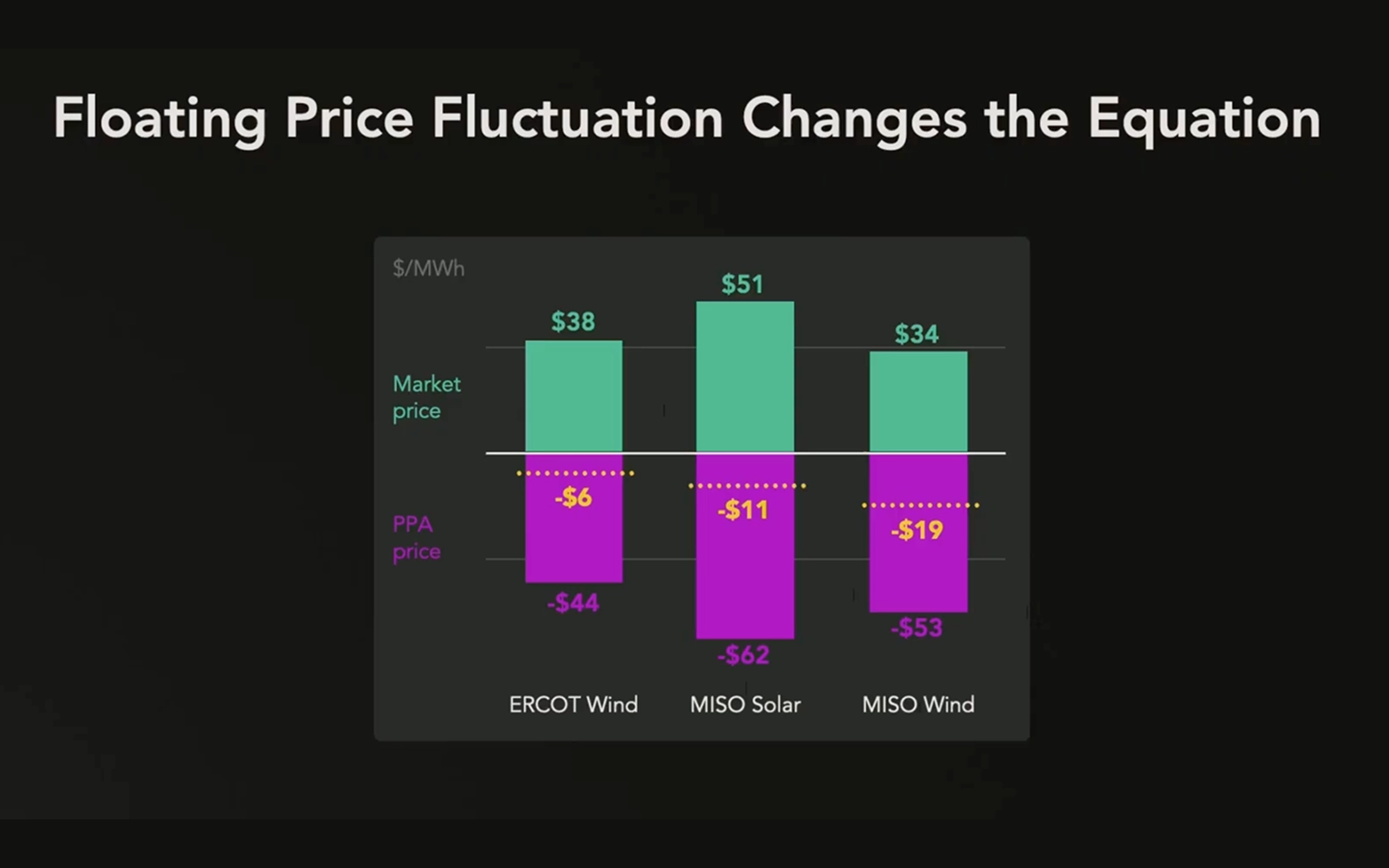

Wholesale market risk occurs in any hour when a company’s electricity use — its load — is mismatched with its supply of energy. The greater the mismatch, the greater a company’s market exposure.

This mismatch can occur in two ways. First, when a company hasn’t procured enough generation, known as a short position, forcing it to top up its supply by paying the spot market price. Second, when a company has procured more generation than it can use, known as a long position, which forces it to sell excess generation into the wholesale market at spot prices.

The first step to managing wholesale market risk is to develop a baseline of forecasted exposure. This is done by combining the company’s forecasted hourly energy usage with a forecast of hourly generation in the markets in which it operates to calculate the net position. Once the net position is calculated, it can be mapped onto a risk heat map to identify areas of high market exposure.

The next step is to specify the company’s risk appetite. This could include capping market exposure by placing limits on long or short positions, capping potential variability by limiting metrics like mean absolute deviation, or specifying a willingness to pay to narrow the distribution of potential electricity supply cost outcomes.

Once a company has quantified its baseline and risk appetite, the next step is to build a portfolio of risk management products to mitigate wholesale market exposure. Verse’s Aria platform combines decades of experience in electricity risk management with real-time price data on all available risk management products. Using sophisticated mathematical algorithms, it provides the optimal suite of risk management products to achieve your organization’s goals at least cost.

The result is a risk-mitigated portfolio with reduced wholesale market exposure, based on your organization’s unique preferences.

Contact us for a demo of our risk management software.